A 101 Class in Web 3.0: The basics (and barriers) of blockchain broken down

-

By

Matthew Rickard

By

Matthew Rickard

- 5 min read

- Aug 09, 2022 1:16:21 am

In this blog post we dig into some the fundamentals of Web 3.0 and where it may, or may not, be of use to you business. We cover:

- Getting past the tech

- The why of Web 3.0

- And the how…

- Learning the Lingo

- How brands can lead the way

- Time to make a change?

Let’s start with the most fundamental question. Not ‘What is Web 3.0’ – but ‘Why might Web 3.0 matter to me?’

There’s a fine line between being a fool for fads and a complete luddite. Embracing new technologies too quickly can result in expensive mistakes – and risk your brand looking naive to its customer base – but then so too can failing to embrace those technologies. The worry is that you’ll either look out of touch or out of date.

Knowing when to engage with an emerging technology can be a difficult exercise; one made all the more difficult by the speed at which they emerge and the resultant skepticism that surrounds them. And in terms of skepticism, Web 3.0 has met its fair share. What is Web 3.0? The terms you’ll have most heard associated with it are Blockchain, Bitcoin and NFTs but getting away from the technical jargon, it’s perhaps better to understand the journey of the internet through its various stage from one to three.

Chris Dixon, internet entrepreneur and partner at a16z where he focuses on web3, has a very simple but precise way of explaining the internet version journey: Web1 was read-only, Web2 is read-write, Web3 will be read-write-own.

With Web 3.0 the clue lies in the word ‘own’ as there is a focus on building community around active, rather than a passive, agents. It’s still evolving but what is clear is that Web 3.0 will have a strong emphasis on decentralised applications and make extensive use of blockchain-based technologies. It will also make use of machine learning and artificial intelligence (AI) to help empower intelligent and adaptive applications.

In many of our blogs we’ve addressed the issue of how the Web 3.0 space seems to be dominated by ‘Crypto Bros’ and ‘Bored Apes’; a very particular stereotype who you definitely don’t want to get stuck in a corner with at a party, lest you want to be on the end of a three hour monologue on the new world order.

The problem is that whilst this stereotype does draw from a sadly true phenomenon, in reality it represents only a very small proportion of the Web 3.0 space – a fact that’s particularly relevant when you realise just how many good things are happening as a result of this mini-revolution; from empowering minority groups and the less-economically-developed communities, to democratising artist engagement, to decentralising financial controls and granting new ways for social enterprises and entrepreneurs to raise capital.

Getting past the tech

Aside from the image element we’ve addressed above, one of the central obstacles that stops the mainstream from engaging with Web 3.0 is the idea that it’s too technologically complicated. Which is saying something when you consider how quickly and easily everybody has embraced technology, to the point that we’re now mostly more than comfortable with the internet running our fridges and even our Grandmas know how to ‘Ask Alexa’.

There is really very little to fear from a technology point of view – there are a range of systems, organisations and platforms in place to make it very simple to engage with. And what makes it a lot simpler is understanding the basic premise underlying it – an understanding that is best developed by embracing the philosophy before the technology.

The why of Web 3.0

When Web 2.0 hit (Web 2.0 being the idea, largely, of social media) the philosophy that underpinned it was that of engagement – encouraging bi-directional participation rather than passive consumption of content on the internet. But it still required the presence of a facilitator – and that’s how the dominant internet forces emerged; Facebook, Google and all the rest. Even though it felt like the power dynamic had been equalised, since people now had a voice – the reality was, it actually centralised the power of these forces more than ever.

Web 3.0 aims to change this. The core value is that of decentralisation – which carries with it the idea of not putting your trust in any single source, and not having to ask any single source for permission to participate – whether that be in terms of creation, contribution or financial participation. All of it functions as a community, albeit a community with highly regulated, controlled mechanisms for interaction.

And the how…

So how does technology contribute to that particular ideal? Well, the normal internet exists on a range of supersized servers located around the world, and owned and managed (or at least rented and paid for) by the big corporations who hold your data on the websites you use. They use their own security systems to grant you space, access or rights to some form of asset, and the relationship exists between you and them. You ask them for permission, and you trust in their integrity.

Blockchain doesn’t exist on any single server. It allows you to keep a record of an asset (which might be tangible or intangible) within a ledger that is formed by adding that asset to a (block) chain of assets that have existed before it, with that chain being formed by the work of a whole network of decentralised computers owned by different people. It’s a little bit like the days of P2P file sharing back in the 2000s, where people spent days downloading a 360p bootleg film from a number of seeds – but it’s a bit more complex (and entirely more legal).

The links of the chain are inherently bound to each other through complex algorithms, which means it’s impossible to go back and alter or take away a link in the chain.

The net result is that your entry on the ledger is immutably fixed, and doesn’t depend on any single source to grant legitimacy. Rather ironically, people think that crypto and NFTs constitute made-up things, when in fact their existence is made far more concrete by virtue of relying on the mechanism that creates them, rather than being granted by a third-party (who could, hypothetically, turn around one day and capriciously announce the non-existence of that asset).

Learning the Lingo

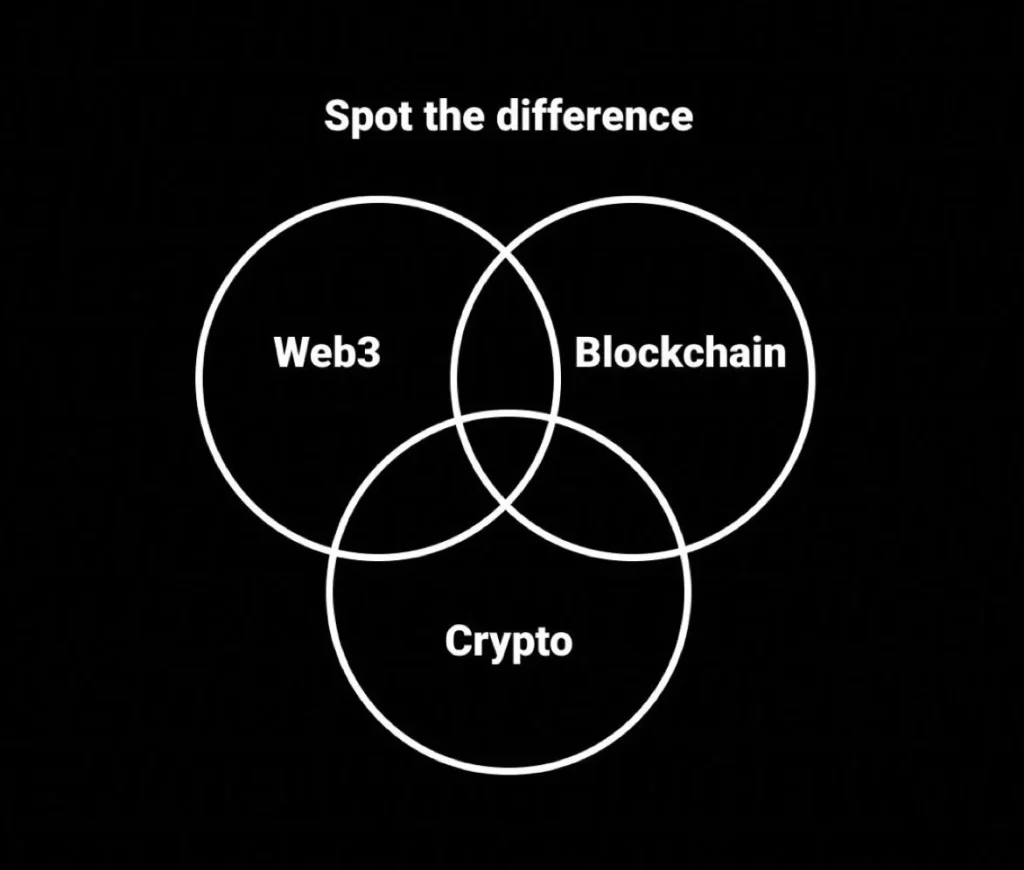

With the principle of Web 3.0 and blockchain established, there is still a question of understanding the terminology associated with it, which is often bandied about by crypt-bros in a way that makes it sound much more complex and exclusive than it really is. The first main thing to get to grips with is the difference between blockchain, crypto and NFTs and the associated technology.

Here is a handy glossary on Web 3.0 which goes into a little more detail, but in essence blockchain is the overarching name for the way of creating the ledger, whilst crypto constitutes the use of that for purely financial instruments, and NFTs represent the ‘all other assets’ that you might creating using blockchain.

It’s NFTs that we at the Blue Marble are centrally concerned with. The media often portrays these exclusively as digital artworks – and certainly this is a significant part of the NFT scene, but it’s by no means the whole story. NFTs can be used to create any non-replicable, exclusive ledger item.

Sometimes that’s a unique ownership right over a digital image (though crucially, not necessarily the unique presentation of that image), but it can also be a carbon credit, or a proof of event – running a marathon, donating to charity, or even a digital equivalent to a real-world property deed.

All of this is generally handled through a digital wallet. These are either hosted, non-custodial, or hardware based. The first – hosted – means that your currency (or asset) is kept by someone else; normally the person you bought it from. In this sense, it’s the closest to a bank – which means it’s convenient and flexible (and all is not lost should you forget your password), but it slightly undermines the idea of crypto being ‘trustless’ and ‘permissionless’ since you still have dependence on a single third party. Some of the more complex areas of crypto might be inaccessible to you with a hosted wallet, but for basic buying, selling and storing crypto, it’s just fine.

Non-custodial wallets give you the software to store your crypto (which, remember, isn’t the storage of money per se, but storage of the ledger entry details needed to point towards your ledger entry on the blockchain). These can make it slightly complex to move crypto sometimes (you can’t always just buy with conventional currency), but they do facilitate more complex crypto processes. But the main thing is, if you forget your own password – that’s it, game over. There’s no-one to request it from. It’s all on you.

Finally, there are hardware wallets. These are for those truly invested in the philosophy of Web 3.0 and the idea of being utterly un-reliant on any third party. It makes them optimum in terms of security (which is incredibly high for crypto in general anyway), but now it’s not just an issue of forgetting your password – if the physical storage is lost, so is your asset (and there have been a fair few stories of people losing their drives – with one person offering millions to his local council if they’d let him search the local dump for his lost $200 million crypto drive. That’s one stinky treasure hunt we’d rather avoid.

Whilst it’s good to know about all of these, the growing accessibility and security of hosted digital wallets means those beginning to engage with Web 3.0 really don’t need to concern themselves with anything more complicated.

How brands can lead the way

‘Mainstream operators are now immersing themselves in the Web 3.0 space (think Nike, Gucci and the NBA, to name a few). And yet to the average consumer the whole concept can still seem a little daunting.

It will fall to brands – at all levels – to make the move, and educate their market as they go. Those that are bold enough to lead the way will own the space and control the narrative – giving them a significant advantage over competitors.

The key to this though will be education; brands framing their use of the 3.0 space to their customers in a way that is engaging, informative and persuasive, but still entertaining and exciting. The right NFT, with the right supporting marketing strategy, can work wonders.

The core of that education must focus on two central things; accessibility and benefit. Accessibility refers to the process of making customers realise that engaging with your branded NFTs is as easy as buying any physical transaction or investment they might make in the real world. It needs to take the mysticism and fear out of the idea.

But benefit is perhaps even more important, and complex. We’ve written another blog here which discusses how NFTs can be used in a way that brings far more than just speculative financial gain. Indeed, framing them only as investments can be counterproductive; the relative novelty of the platform means it still feels daunting and uncertain to first-time users, who would feel far more confident investing their hard-earned cash in traditional stocks, savings or investments.

However, if you frame the benefits of your brand’s NFT as more than merely financial; using NFTs as membership that delivers ongoing exclusive perks, creates a sense of community and belonging, and creates a wider societal benefit too (which we cover in more detail here) – then your base will feel both more confident and motivated.

Time to make a change?

We posed the question at the beginning – how do you know if it’s time to get involved in the world of NFTs?

We’d say the clear signs are:

- The technology has matured and simplified, with a range of applications making it accessible to the general population

- Mature, established and market-leading brands are integrating it into their core branding and marketing activities

- The trendy faddishness of its initial rise has passed, and what has subsequently emerged is a space that can produce meaningful change

- But the space is still new enough that there is a role for brands to pioneer as thought leaders and meaningful agents of change

If you’re looking to take the first steps in integrating and NFT strategy into your brand, why not contact us at The Blue Marble to talk about the path ahead.

{{cta(‘4c4de3d7-3565-40f1-899d-f2e9febf5d2f’,’justifycenter’)}}